ATFX is on a hiring spree – read about it here.

Naga is a company whose accounts we once looked at with a feeling of trepidation (also one of my personal favourite headlines). A lot has changed since then.

Readers probably don’t need to be told that rival firm Capex bought out the broker, which was loss making, via a reverse merger. That has now received regulatory approval and the two companies are in the process of becoming one. This means Naga-Capex will continue trading on the Frankfurt Stock Exchange.

On the back of the merger going through, the founder of Capex – Octavian Patrascu – gave a capital markets update to shareholders. There were a few interesting points within this, so I figured we’d go through them.

Speak to Centroid Solutions about your bridge and risk management technology.

1. Why did Capex and Naga merge?

When we spoke to XTB CEO Omar Arnaout recently, one of the points he made was that XTB would consider acquisitions if they either (1) improved the company’s product or (2) added additional licensing. In IG Group’s recent capital markets day, CEO Breon Corcoran said exactly the same thing.

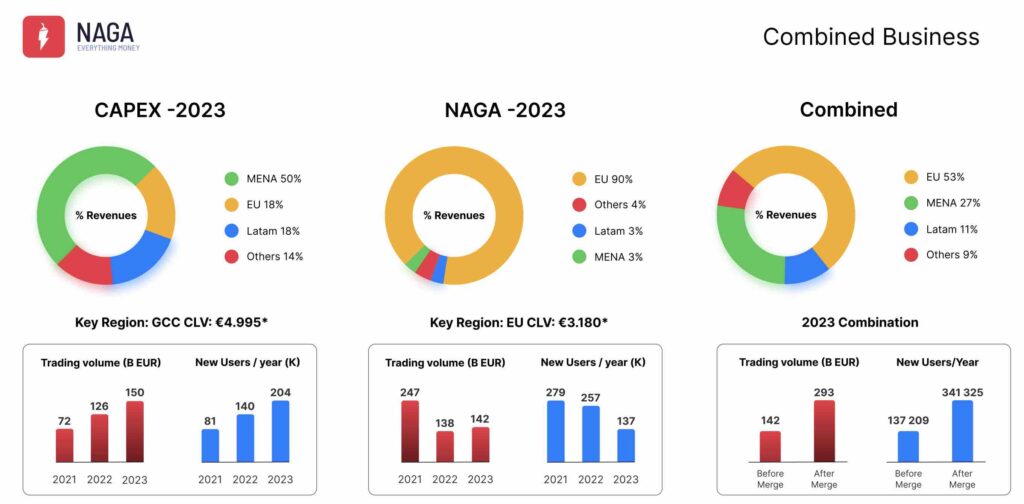

So it probably shouldn’t be that much of a surprise that Capex bought out NAGA because it had products it wanted and also because it had geographical reach that it didn’t have.

Capex, like a lot of brokers, has been very successful in emerging markets. In contrast, 90% of Naga’s revenue was from the EU in 2023. At the same time, Capex has only got a CFD offering but Naga has crypto, payments, copy trading, and cash equities. You can see this in the slide below…

2. Everything money

The new slogan that the company is going to use is ‘everything money’. Kind of corny but it gets the point across. The idea is that you can use Naga for all your trading / investing / money management needs.

This is basically what every big player in the industry is doing and they pretty much all want the products that Naga has, so maybe this will look like a good acquisition in hindsight.

Another point that Patrascu made was that different products could be used to cross sell each other. Again, this is not likely to be news to anybody. When we looked at how XTB and Trading 212 got so big a few weeks ago, the answer seemed to be that offering stocks meant they could onboard a lot more people, particularly during Covid.

What will be interesting to see is how viable a route to acquire customers this is moving forward. Ultimately any broker doing this is using it as a marketing tool. Other products have lower CACs, which means (hopefully) you can cross sell a customer CFDs, having acquired that customer at a lower cost.

But if you think of the CAC as being driven by something akin to an auction, the more companies have these products, the more the CAC gets driven up because everyone just ends up bidding for the same ads, exactly like they do with CFDs.

3. Influencer effect – John King and Capex

One of the minor points in the presentation was some information on the campaign Capex undertook with John King. I thought King was an unusual choice as he’s in the US but apparently the campaign got >80m views.

Given you are all a utilitarian, reductionist bunch, I know your next question will be ‘but how much conversion did they get from it?’ – alas, there was no detail in the presentation on that point.

4. Capex made 18% of revenue in LATAM and is applying for a Chile license

One of the standout points in the presentation was that Capex generated almost 20% of its revenues last year in Latin America.

In real terms that was just under €7m. We have seen lots of firms targeting the region and, although this is obviously not an insane amount for big industry players, it’s still interesting to see that they are doing a decent amount of business in the region.

It’s also worth noting that (1) XTB’s CEO said Chile could end up being one of its best branches and (2) that was one of the countries they were looking at getting regulated in next. Pepperstone has also opened an office in the country within the last 12 months and Capital.com is targeting customers there.

5. Other broker executives involved

There are a few technical parts of the Capex-Naga merger that are interesting. One is that Eyal Wagner, who was part of the senior management team at Markets.com, is now a board member.

Another factor is that Capex is itself partly owned by a VC called Growthbox Ventures, which is based in Malta. Growthbox also has stakes in Skilling and Nextmarkets.

I don’t know what the normal holding period is for Growthbox but it might be they just end up cashing out after the merger. The potential problem there could be liquidity. At this point in time, the free float for Naga is less than 10%. Note that this ‘problem’ also exists, for different reasons, for XTB and CMC Markets, although it is far less extreme in both cases.

6. Why Naga is the brand they’re going with

Naga, Capex, Nagex, Capanaga – the whole time I was watching the presentation, I was wondering what the company would actually be called post-merger. Apparently it’s Naga.

Patrascu’s explanation was basically that Naga invested more in brand than Capex and Naga also ranks better in Google. Some other (unmentioned) analytics were also used to reach the conclusion that Naga would be a better option.

7. Options and an EMI license

A couple of other points in the final Q&A were also interesting. One is that Patrascu said the company would add an EMI license if possible. The other was that the broker would consider adding options down the line. However, the fact that a Naga customer asked this was probably more telling than the response. People seem to want to trade options, something I’ve said here for a while.