Last week on TradeInformer we published an interview with Filip Kaczmarzyk, Head of Trading at XTB.

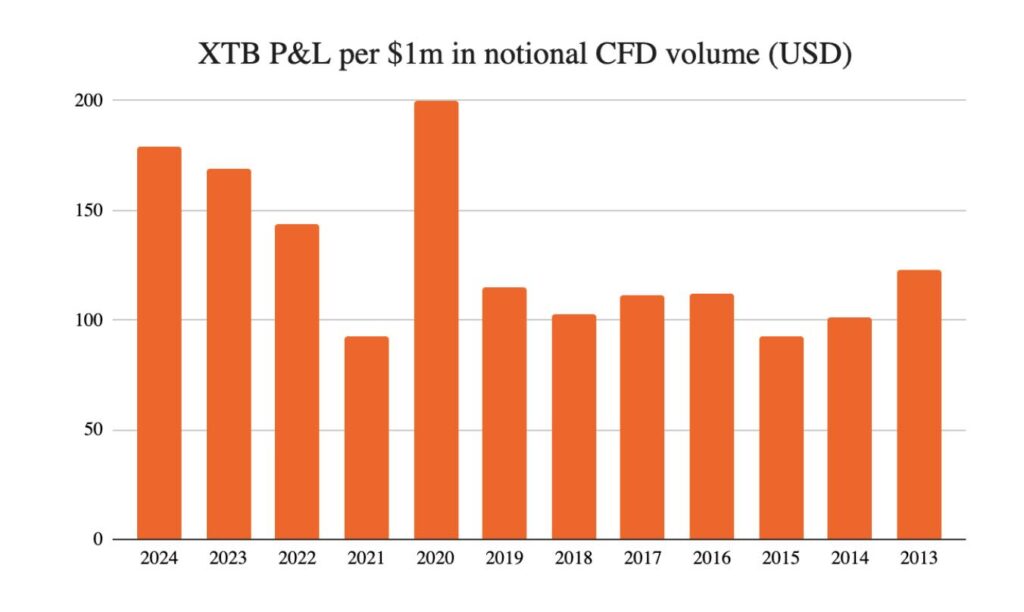

One of the questions I put to Filip was whether XTB’s growth means the company has been able to internalise more flow and thus generate a higher level of profitability per $1m of notional CFD volume traded.

As you can see below, this has risen at XTB over the last decade…

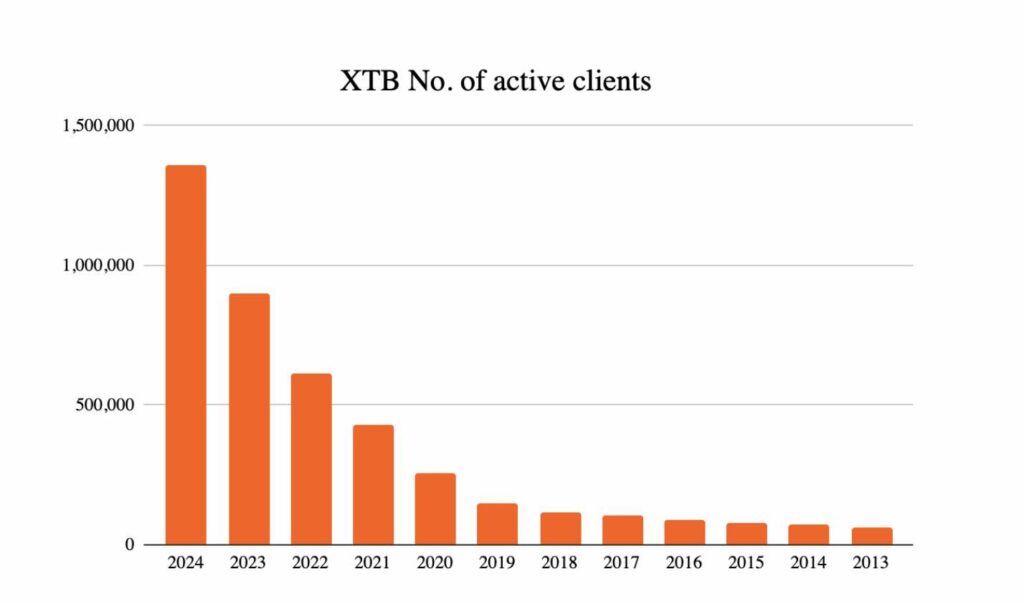

….at the same time as the number of active clients has skyrocketed:

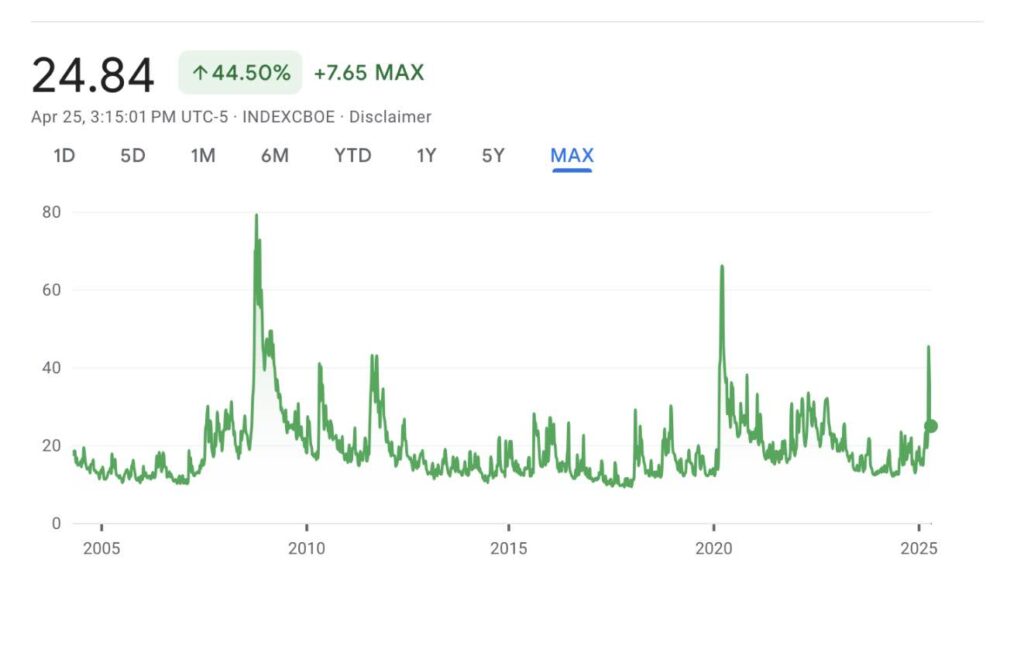

Filip’s response was that the increase was not due to client growth but more volatile markets. And although it’s not a perfect proxy for it, you can kind of see this from the VIX…

Generally you can read across from the performance of one broker to another, so we can assume that the P&L per lot of most brokers bears some resemblance to the profitability of XTB in the chart above.

What to make of this? I generally think technical analysis is…well I won’t use the word.

However, what I think does (arguably) make sense is mean reversion within low volatility, range bound markets. I’m sure some of you nerds will disagree but markets are moved by information or liquidity events.

The latter is not the same as the former as it should (in theory) have no bearing on price.

For example, let’s say I’m Crispin Odey and I own 10% of Plus500. I get caught up in a sex scandal and have to close my hedge fund. Now I have to return funds to shareholders, so I have to sell my shares in Plus500.

This scenario has no bearing on Plus500’s value. But it will have market impact because you are dumping a bunch of shares in the market. So in theory, you would expect a fall, and then rise again as the price reverts to some mean value. There has been no informational change that would shift prices to a different level.

Stuff like this is what is moving markets up and down all day. Some random pension fund has to swap dollars for pounds or an airline has to hedge its exposure to the oil price.

The reason this is relevant to brokers is that, when you look through most automated trading strategies, they are essentially predicated on taking advantage of movements in price that are not informational, but liquidity driven.

For example, go and look through the cTrader store and you will see that a lot of the bots are basically mean reversion tools or provide the ability to make a mean reversion strategy. You can also see the impact on brokers in the XTB P&L chart above.

The interesting question for brokers then becomes is it good or bad to sit on the other side of these trades? My answer is yes.

The big problem, you will have noticed, with mean reversion is that it does not take into account big volatility events. To use nerd language, it assumes Guassian distributions apply to markets, which (I think) they don’t. Or to use simple language, markets blow up once in a while and your EA will blow up too if you are using one of these strategies.

The result is that brokers, without trying, become something like a tail risk hedging strategy by taking on mean reversion trading strategies. For those unfamiliar with tail risk hedging, it’s usually achieved by buying out of the money put options continuously. You bleed small amounts of money and then when markets crash, you make a huge return.

The same principle applies to mean reversion. These strategies pick up small amounts regularly for a long time, then completely blow up when there is a crash. It’s like the ‘picking up pennies in front of a steamroller analogy’. Brokers get to be the steamroller.

However, there is an obvious potential problem here, which is that sometimes markets can stay range bound for a long, long time. As the XTB chart shows, sometimes it can be years.

Here the risk becomes obvious. If you are dealing with someone that is taking money from you regularly for a prolonged period of time, do you have the balance sheet to be able to deal with them?

The larger brokers obviously do and it’s why so many of them are able to warehouse the flow of lots of clients like this for long periods of time.

Others do not. And for those that don’t, it raises the question of whether you should keep booking these people’s trades or send them to the LP.

To use an analogy, I remember in my previous job talking up a fund we were selling to a curmudgeonly co-worker. The fund had underperformed badly because the managers refused to invest in a set of specific companies that were driving all the performance in the sector they specialised in.

“It’s not that bad I said, they’ll be right in the end and it’s only been two years,” I said.

My curmudgeonly co-worker just looked at me for a second and then shouted…

“Two years!”

Then he went back to work. Now that fund is going to wind up.

My point being, you may be right in the end, but if you don’t have the balance sheet then you could die waiting.