Long term readers of this newsletter may remember some of the early pieces written here about the case for investing in Plus500 and CMC Markets. The short version is that CFD providers tend to have low valuations but good growth potential, no debt and impressive operating margins.

One company that I have looked at intermittently but never in great depth is Naga, which is listed on the Frankfurt Stock Exchange. Although the group has an entity in Germany, the majority of its employees and operations are in Cyprus.

Some readers may be familiar with the problems the company had with its accounts in the past, where the auditor (EY) was capitalising affiliate marketing costs, something it was not permitted to do under IFRS accounting standards.

To be fair, Plus500 has had a much more dramatic accounting lapse since being a publicly traded company and plenty of businesses have hiccups like this. Naga also fired EY, its prior auditor, and hired a new firm to do its accounts. However, looking through their latest accounts you wonder if maybe they should also fire them as well.

Look at the income statement alone from the most recent half-year results and you start to notice some peculiar things.

First there are the dates:

As you can see from the text at top, the period under review is supposed to be the first six months of 2022. However, the date listed below as a column header is from the start of 2021 to the middle of 2022 – ie. 18 months. So the dates are wrong.

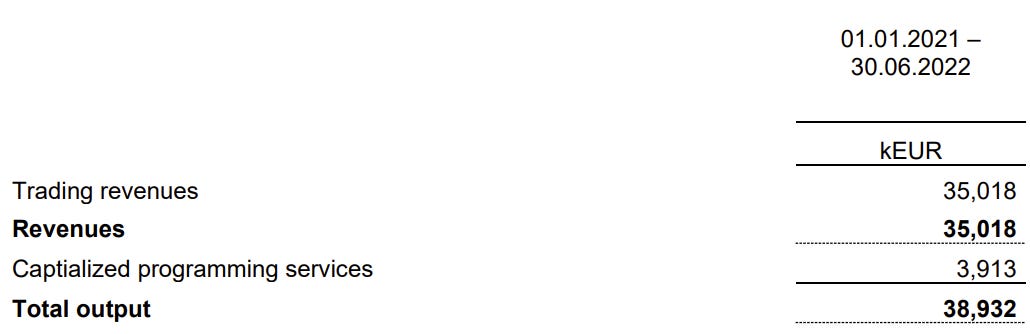

Then we have the firm’s main revenues for the six month period:

Readers may notice that….

Revenues = 35,018

Capitalised programming services = 3,913

Total output = 38,932

But 35,018 + 3,913 = 38,931

The likelihood is that there has been a rounding error, something which the company says may be present in the accounts, but it is still not a great look. Also note that capitalised is spelt incorrectly (“captialized”) in the accounts.

Readers may think all of this is nitpicking. Fair enough. But the next point is harder to put into that category.

If you look at the above image again, note that revenues are added to capitalised programming services to form something weirdly named ‘Total output’. Capitalising costs is a common accounting practice but Naga has undertaken it in a peculiar way.

To summarise, if you are a company, you may not want to have the money you’ve spent developing software listed as an operating expense on your income statement. The kind interpretation of this is that you have effectively exchanged money for an asset, one that will hopefully increase your revenues in the future, so it makes sense not to expense it. The less kind interpretation is that you want to improve your profitability.

Instead of listing an operating expense, you decrease the relevant amount of cash on the balance sheet, then increase your assets. If it’s software, most likely it will be an intangible asset. This would also show up in the cash flow statement as an outflow equal to the amount it cost you. Finally, you would amortise/depreciate the cost in the income statement over a set period of time.

To give a very simple example of this, imagine you want to be an ice cream man. You set up a company and put £10,000 into it, then use £5,000 to buy an ice cream van.

Instead of reporting that as an operating expense, you reduce your cash holdings on the balance sheet by £5,000 and increase your fixed assets by £5,000. You report an outflow of £5,000 in the cash flow statement. Assuming you’re using the straight line method, you depreciate the cost of the ice cream van by £500 on the income statement every year for 10 years.

Naga has done the above except they have added the expense on to revenues to form what they nebulously term ‘Total output’. They then calculate their profitability for the period based on the ‘Total output’ figure, as opposed to revenue.

To understand what this means, go back to the ice cream van example. You have bought the van but are too lazy to be an ice cream van driver. You go to fill in your accounts. Your revenue is £0 but you add in ‘capitalised ice cream van costs’ of £5,000. Your ‘Total output’ is £5,000.

If you were to follow the logic of Naga’s accounts, this would mean you ‘made’ £5,000 in sales during that period. But obviously you didn’t, you just spent £5,000 on a van. So at best you have an asset worth £5,000, £5,000 in cash and revenues of £0.

It’s plausible that I have got this wrong. Naga includes ‘development costs’ for IT as an operating expense for the period. However, it’s unclear if that is inclusive of the capitalised cost used to form total output, or if they are separate. Reading through the notes to the accounts, it seems like it is the latter, which would mean there is no offsetting taking place. That view is strengthened by looking at the investment in intangible assets component of the cash flow statement.

None of the three major listed brokers in the UK structure their accounts this way, in fact I’ve never seen ‘Total output’ on an income statement anywhere before. Plus500 (whose accounts are extremely clear) treat software development as an operating cost and CMC, a far larger business than Naga which has also spent large sums on software development, capitalises far smaller amounts of that investment in its accounts relative to Naga.

Another option is that this is some kind of local accounting method. But these were purportedly put together under international accounting standards, meaning it’s hard to see how that would be the case.

My view is that it’s plausible Naga’s auditors have added the ‘Total output’ figure to improve their topline revenue and gain all the other benefits that come with that – higher net income, EPS, shareholder equity, and reduction of cash burn. As with most posts here, I’m happy to be corrected.