Broker Brunch: An exclusive event for brokers in Limassol on April 16th

In February, UK asset manager Schroders published some research looking at the retail investor market.

Most of the piece was designed so they could talk their own book and shill the benefits of active management.

But a byproduct of their efforts was some great data on uptake of investment accounts among retail traders in the US, as well as their behaviours.

With regard to the latter, one of the things that struck me – always anecdotally – in my last two jobs was that retail investors seemed to behave paradoxically.

They would say that active management was dumb and buy ETFs. But at the same time they would also punt on loads of individual stocks themselves, presumably because they are smarter than the active managers they enjoy maligning.

As I said, this was anecdotal for me but Schroders research seems to show that is really what is happening. In the US, people are at close to record levels of direct equity ownership. At the same time the level of ETF ownership has also risen substantially too.

Another crazy factoid was the fact that the number of accounts at the big US stock brokers has more than doubled over the last decade or so. In 2016, less than 40m Americans had a stockbroking account. Today it’s over 80m.

Get a Match-Trader server today

Note that many of these accounts also provide direct access to derivatives trading, which has also exploded.

You can see this in Robinhood’s accounts for last year, where the company generated $760m from options trading – more than any other asset class and up 50.4% and 55.7% on 2023 and 2022 respectively.

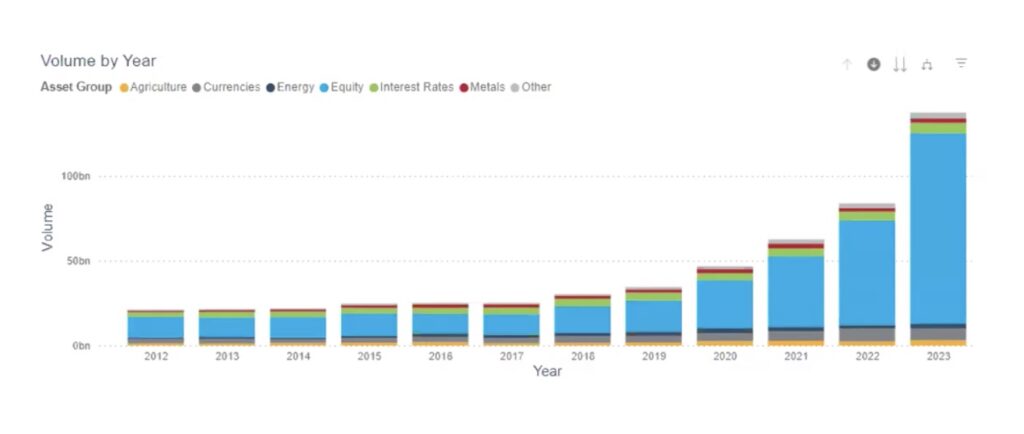

More broadly, you can see that demand for derivatives trading globally has risen massively over the last decade.

Over in the crypto markets, the rise – from nothing – of companies like Coinbase and Binance has arguably been more impressive. Binance now has more than 250m registered accounts. The fact it could pay a $4.3bn fine to US authorities and keep going is a sign of how large the company has become.

The huge increase in the number of accounts (and revenue) at companies like Trading 212, XTB, and eToro suggests European customers have been part of these trends too.

The point I’m making is that the general movement over the last decade has been for retail clients to become more and more interested in speculative financial products.

Where Europe stands out is in attempting to stop companies from facilitating this and pushing clients to offshore firms.

Spain’s marketing ban on CFDs was one sign of this. Over in the UK, the underlying logic of the Consumer Duty regulations seems to be that the only acceptable service you can provide to a client is one where they make money, something that makes no sense if you are in the business of let people take on financial risk.

ESMA’s restrictions on leverage were another component of this. Not only did these have zero impact on outcomes for clients, they also pushed huge numbers of them offshore.

For example, one broker that I spoke to recently said they lost half their client base overnight after those regulations came into play. I also regularly hear from firms who note that clients will just go for an offshore firm if they don’t get the leverage they want.

Stop getting arb’d, start using Centroid

The way that European regulators think about this stuff was – in my view – perfectly captured by Peter Kerstens, an advisor on the latest (and also bad) MiCA regulations.

“if you are a crypto service provider in a foreign country, minding your own business and not doing anything to attract business from the EU, and some EU person walks into your virtual crypto shop and wants to buy your wares, there is nothing EU authorities can or should do about this.”

Great.

To be fair to European regulators, and perhaps regulators more broadly, riskier products pose something of a conundrum.

Regulators are often tasked with helping to foster growth and innovation. At the same time, if you have lots of clients signing up for risky products, you are almost guaranteed to have lots of complaints.

If you take CySEC as an example, they have about 120 people working for them. If they have 150 companies under them, it must be extremely hard to actually manage all of them, not because CySEC is ‘bad’ but because they don’t have the resources to do it. The same is true of the FCA or ASIC.

So you are stuck in a situation where you have to grow an industry that (arguably) causes problems which you don’t have the capacity to manage.

Nonetheless, the changes just keep coming.

In the last couple of weeks, CME Group has launched a suite of spot price futures that look a lot like a CFD.

You are also seeing Kalshi and Interactive Brokers push hard on launching more intuitive binary option products (or ‘event contracts’). Both firms have faced some lawsuits or are launching their own so that they can offer the products. They will win in every instance because the US government will want to support them and then they’ll push on to offer them abroad.

There are lots of things regulators across Europe could do to cater to demand for higher risk products and offer protection to clients. We’ve looked before at the idea of not allowing passporting of CFDs, for example.

But the key problem seems to be mentality. Much of the world seems to embrace a ‘buyer beware’ culture.

In Europe that’s not the case. To take an example from a different industry, everyone today knows that smoking is bad for you. But in Europe they still felt it was necessary to do plain packaging as well. In the rest of the world the mentality seems to be more like ‘well, you knew what you were doing, deal with the consequences’.

Sadly that probably won’t change. Taking personal responsibility isn’t the European way. Time to get a Vanuatu license!