eToro was supposed to go public last year via a merger with a special purpose acquisition company (SPAC) at a $10.4bn valuation. That was later watered down to $8.8bn in the final days of 2021 and the deal now only has until the end of June to go through.

Nothing in the intervening period bodes particularly well for the company. The sky high valuations that we saw emerge over the past couple of years have come crashing back down to earth and it’s difficult to see that changing in the near term.

The SPAC bubble was almost guaranteed to be burst at some point too. Without going into the finite details, SPACs to me seem like scraps of financial engineering largely designed to benefit their sponsors and initial investors, the latter of whom, by redeeming their shares and holding on to warrants, effectively get a risk-free trade.

Leaving those problems aside, and regardless of what happens, it’s still worthwhile looking at whether or not eToro deserves the $8.8bn price tag it’s hoping to achieve. My view is that it doesn’t.

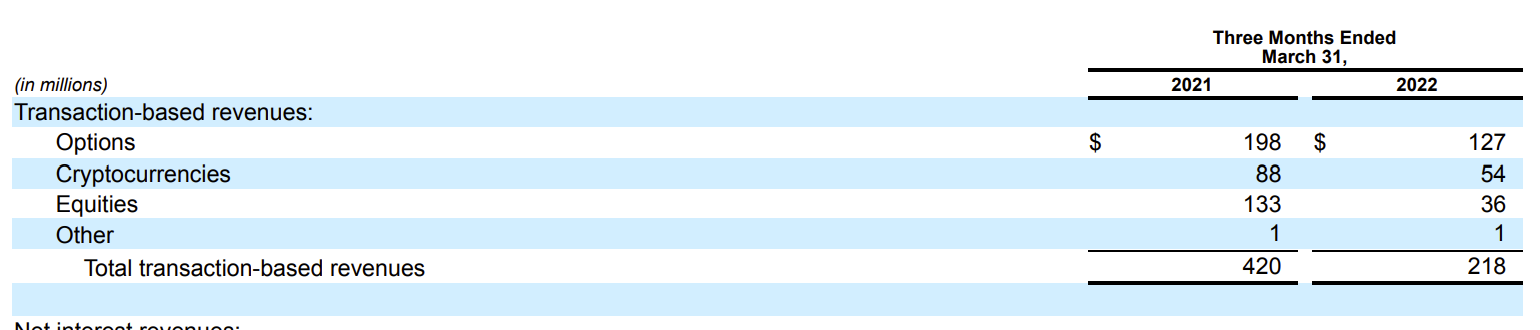

Many valuations of the company have drawn comparisons with Robinhood, which is now trading with a market cap of, funnily enough, $8.8bn. I don’t know if this is the most apt comparison to make. As you can see in the image below from its latest quarterly report, Robinhood mainly makes money by selling order flow, with most of that cash coming from options trades. It’s also only active in the US for now.

eToro doesn’t offer options, although it has started selling order flow on its equities offering in the US. It also only makes about 14% of its revenues in the US. The vast majority of its earnings – 69% – come from the UK and Europe.

eToro may one day look like Robinhood and have a large US customer base that it makes money from by selling order flow. But for now it doesn’t, so comparing them to try and determine a valuation isn’t quite right.

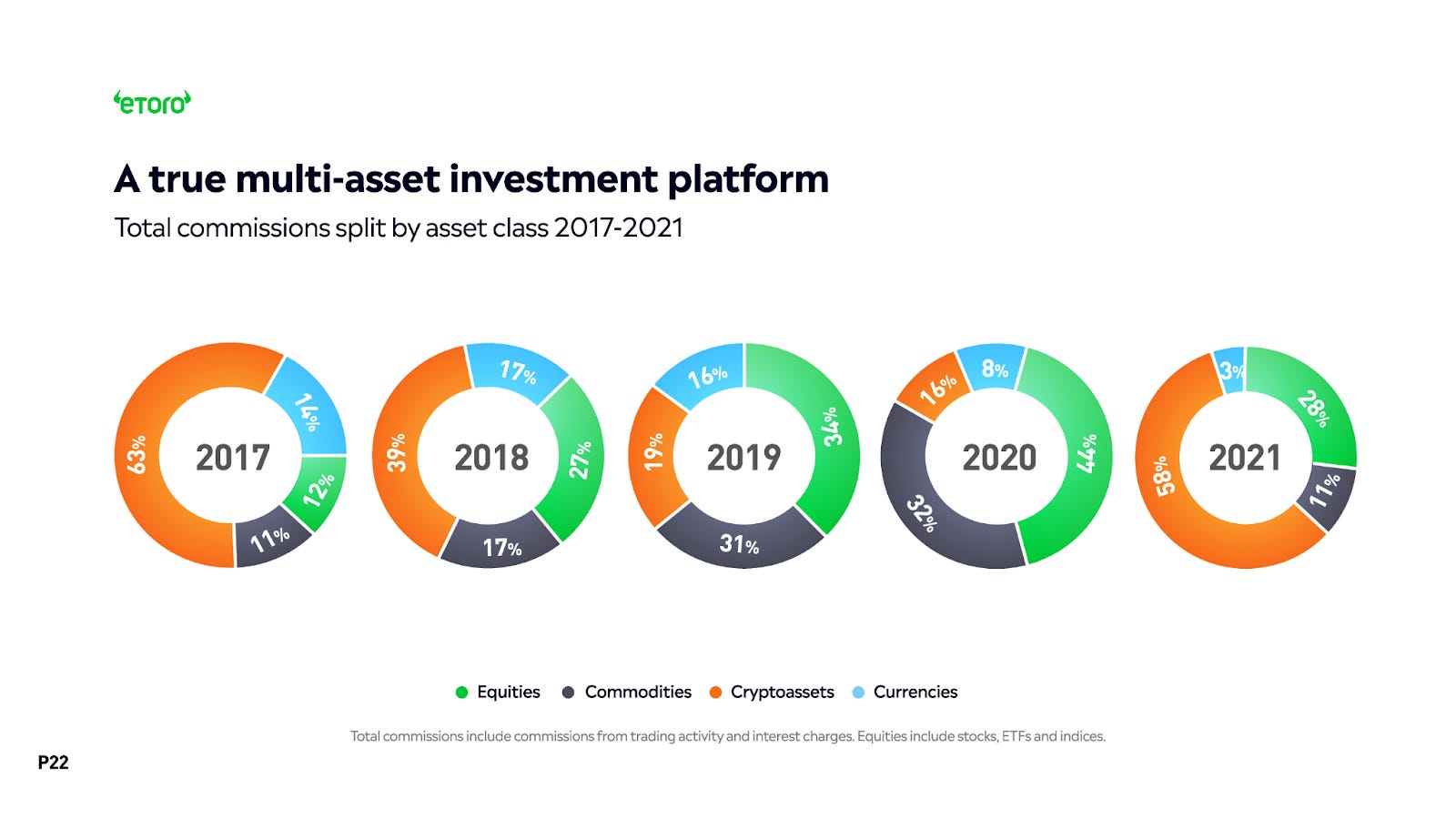

Unfortunately, working out how eToro does actually make money isn’t easy. Looking at its most recent full-year report shows us a 5-year revenue breakdown as follows:

The annoying thing about this is it doesn’t tell you how the clients traded those assets. Some clients can trade all of them as CFDs, whereas others, in the US and UK for example, can’t. Stocks and cryptocurrencies can be traded as the physical asset but also as CFDs.

The company states that in 2021 it had:

- Total funded accounts of 2.41m

- Trading revenue of $1.23bn

- Has AUM of $10.7bn

As I wrote when discussing CMC Markets a few weeks ago, pure play stockbrokers make about 40bps to 50bps on their AUM. eToro is making almost 25x that amount. To break that down further, it means that the average account size is a little under $4,500 but the average revenue per customer is around $500. For comparison, that is how much IG Group made, on a per client basis, from its share trading service, with account sizes almost 10x as large.

What that means is eToro clients generate revenue more like CFD clients than they do stockbroking ones. On that basis it seems more reasonable to compare eToro, for valuation purposes, to its listed peers in the UK, like IG and Plus500.

IG is currently trading with a market cap of £3.1bn ($3.8bn). The equivalent figure for Plus500 is £1.50bn ($1.85bn).

Plus500 is, in my opinion, the standout listed CFD provider and is severely undervalued.

Last year the company employed 400 people. It delivered $718.7m in sales and $387.1m in EBITDA. This means the company made close to $1m per employee in pre-tax profit.

IG Group has a slightly odd financial year ending in May. In its last full year, with 2,054 employees, it made £853.4m ($1052.7m), with EBITDA of £450.3m ($555.7m).

eToro employs 1,800 people – 4.5x as many as Plus500 but less than IG Group – and produced $1.23bn in revenue last year, with losses of $265.7m.

Looking at these stats alone, it’s hard to understand how eToro can be worth substantially more than either IG or Plus500. Advocates for the company would likely argue:

- eToro is a fast growing business, whereas IG Group and Plus500 aren’t. Future earnings justify a higher valuation as a result.

- eToro is loss-making because of its high-marketing spend. It can cut this and become profitable in the future.

The trouble with this is that IG Group and Plus500 are also making big efforts to expand. IG Group spent $1bn on acquiring TastyTrade, a US options trading company, last year. Plus500 also bought a US derivatives trading business, Cunningham Commodities, and a Japanese broker, EZ Invest Securities, in the past 12 months. It has also launched equities trading in Europe and is about to do the same in the UK.

In short, both companies are clearly looking to expand and have cumulatively spent billions of dollars trying to do so. Thus the idea that eToro should be worth more because it’s going to expand doesn’t really hold water – so are Plus500 and IG Group.

The other point pertains to eToro’s marketing spend. This was $561m last year – a substantial amount of money. Cutting back on this would mean the company could move towards profitability.

This poses some problems. One is that if eToro is going to keep expanding, and that’s what it has said it will do to prospective investors, then it will need to keep spending on marketing. Cutting back on marketing may harm growth, which is what the company’s high valuation is based on. So there is something of a cyclical argument there.

Then you have to question how much the company could cut back its marketing spend. It’s probably fair to assume that it would not be zero but would it be by 25%, 50%, or more? It’s an unknown and, until eToro shows by how much it can cut spending, anyone making the claim that they can do so is just guessing.

The other problem with eToro’s marketing spend is they aren’t getting much bang for their buck. As noted, the average eToro customer made the company about $500 last year. This is substantially less than the $1,764 that Plus500 made per customer in the same time period and far below the £3,690 that IG Group made from its derivatives customers.

Why does this all make me think eToro is unlikely to get a $8.8bn valuation or, at least, make it last for long?

IG Group and Plus500 are both worth substantially less than that despite the fact that:

- They both have growth plans as compelling as eToro’s.

- They have actually proven that they can be extremely profitable, with very impressive operating margins. Maybe eToro could do this but hasn’t proven that it can.

You could argue that it’s not that eToro is overvalued, it’s just IG Group and Plus500 are very undervalued. There is some merit to this argument, particularly with Plus500 that, as I said, I think is extremely cheap based on both its P/E ratio and prospective earnings growth.

But would Plus500 be worth $8.8bn – a nearly 5-fold increase on its current valuation? Maybe at a stretch but it would be extremely pricey if it was. If the company manages to grow substantially in the US and Japan, it may justify hitting that valuation but we have almost no inkling as to how much money it’s going to make from its new businesses in those jurisdictions.

It’s a somewhat similar story with IG Group. The company’s fortunes, in terms of upping its valuation, are now very much tied to TastyTrades. If the latter can grow revenues substantially, then it could push up IG’s valuation. However, it would have to produce a lot of sales growth for the firm to hit $8.8bn.

I totally understand why eToro has gone for such a high valuation. Anyone going public wants to maximise the amount of money they can raise and help existing shareholders cash out at a high share price.

But understanding that’s the case shouldn’t mean we have to go along with it. And for me, the company is not worth the amount they’re saying they are. Investors may agree and we’ll likely see further compressions in its valuation if they do.