Get more IBs and clients with the cTrader Store

Investments broadly fall into three categories.

Something costs a lot because it is going to grow a lot in the future (big tech). Other companies cost an average amount because they have sustainable cash flows but probably won’t grow that much (banks).

Then you have companies where things are going wrong and you need to do a turnaround play. These companies are cheap.

NAGA was a turnaround play for the CAPEX team, who took over the company via a reverse merger last year.

Looking for a new LP? Talk to ATFX Connect

If you look over the last couple of years, there was one point where NAGA had to raise cash via a convertible bond, which only had a six month term but an 11% coupon.

The basic problem with the company was one that afflicted many start ups over the last 10 – 15 years – they made great products but were unsuccessful at monetising them.

In a low rate environment, this could continue for a long time and, if you were able to cash out via an IPO, you could make money from it as an owner. Now rates have gone up, things are different and it is harder to keep raising cash unless profitability is on the horizon.

The takeover of NAGA by CAPEX was thus a bet by the owners of the latter company that they could buy the former for a comparatively cheap valuation and turn things around.

Get a Match-Trader Server today

The pair had licenses and regional revenues that complemented the other. But the main logic of the deal seems to have been that NAGA had good technology and products, whereas CAPEX had better marketing and operations / finances.

Or as the Pet Shop Boys sung…

I’ve got the brains, you’ve got the looks

Let’s make lots of money

Get Social Trading on your platform with Brokeree

Last week NAGA put out a presentation that gave an overview of its finances for the 2024 calendar year. We looked at this report on TradeInformer at the end of last week and some of the interesting points were…

1) 8% of new clients came from Telegram

2) 38% of revenues came from the GCC

3) GCC clients had the highest lifetime value, of over >EUR 5,000

What we did not look at more broadly is whether NAGA could end up being a great investment for the new owners of NAGA.

There are reasons to think that could end up being the case.

All products in place

The basic logic that has developed over the last decade for most brokers is to have your own app / platform and then put all products into that app.

Those products are usually…

1) CFDs

2) Cash equities

3) Crypto

4) Payments

You could add ETDs to this list as well but those four are the main ones that people (brokers?) want.

NAGA has all of those and its own app / trading platform, which tends to be the most capital intensive part of developing these products.

It is also (to my knowledge) the only company that currently has all of its products in one app. If you use eToro for payments, for example, that is not within the main eToro app – you have to get a separate one. Trading 212 has payments within its app but does not offer crypto.

Another way to think of this is that NAGA previously spent huge sums of cash developing all these products but couldn’t continue to the next phase of monetising them.

CAPEX injected $15m into NAGA, with $9m coming from new CEO Octavian Patrascu via a zero coupon convertible bond and the remaining $6m coming in cash from Key Way Group, the previous holding company for CAPEX.

The merger resulted in the issuance of 170.6m shares. Previously NAGA only had 54m shares(!), so this was massively dilutive for existing shareholders but is pretty great for CAPEX’s owners, who now control the business.

So the question then is, would you pay $15m to have…

1) All the products NAGA has

2) All the licenses NAGA has

3) The brand NAGA has

If you think that IG just paid £160m for Freetrade, which makes less in revenue terms than NAGA does, it doesn’t seem like a bad deal. The obvious caveat is that Freetrade is a different product and (arguably) has better growth potential.

Moreover, the reason that NAGA was so ‘cheap’ was because it continued to burn through lots and lots of cash.

The job of the new owners is thus to take a company that had something like £1 going out for every £0.80 coming in. To do that you have to increase the latter number, decrease the first number, or do both. NAGA’s new owners are trying to do both.

Firstly, they have cut headcount by 24%, with a nearly commensurate 21.6% reduction in staff costs. They have also reduced trading costs, outsourcing costs, and other non-disclosed operating costs. Overall operating costs, which includes staff’s wages, were down almost 20% in 2024 compared to 2023.

The next step is making marketing more efficient and increasing the value of clients, firstly by getting bigger deposits and secondly by increasing the ‘lifetime value’ of the client. Or in simple terms – the revenue generated per dollar of marketing spend goes up.

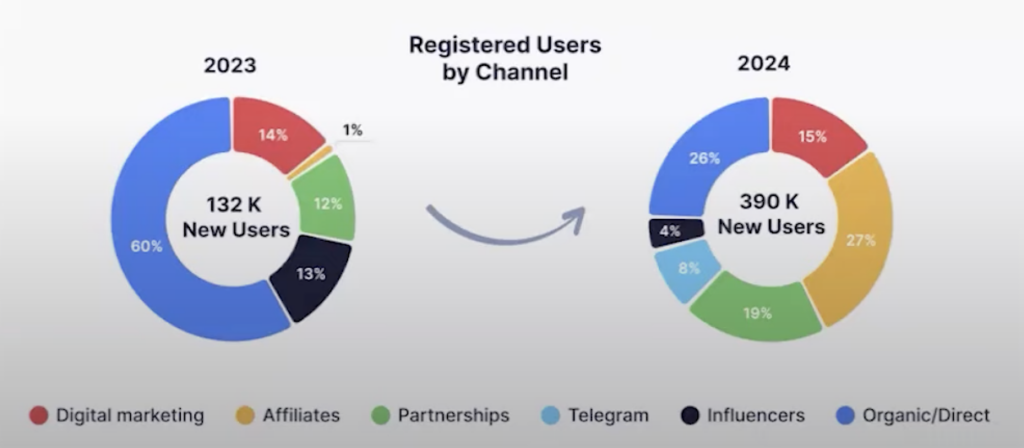

There are some signs that this is happening (although it’s early days). One is a change in the marketing mix. NAGA relied heavily on organic traffic in 2023, potentially because it didn’t have the cash to burn on other marketing channels. Regardless, as you can see below, the mix of channels is now much broader.

The other factor was that the lifetime value of clients rose from EUR 3,000 to EUR 3,340 – an 11.1% uplift.

NAGA only fully completed its merger and unified under one brand towards the end of Summer last year. Consequently there is not much to go on here. There are early positive signs but we’ll have to wait and see what happens.

The other thing to watch is NAGA’s cash flow statement, which we don’t have a full picture of yet.

NAGA was previously making massive investments in technology, then capitalising them on its balance sheet. The result is that the company continues to have huge amortisation / depreciation figures that reduce its overall profitability, even if ‘real’ money is not actually leaving the company.

The company has said that last year saw it reduce cash burn to break even point, meaning the company is self-sufficient in driving its own growth.

Another point to watch here is debt. The NAGA team said the company now has no debt but does have access to a $10m loan, which will only be used for M&A. The terms of that loan haven’t disclosed yet but it sounded more like an RCF than financing for immediate expenses.

This would (if things go well) presumably be accretive to returns. The company also says it wants to add spread betting, which implies it will get an FCA license – so who knows? Maybe the loan will be used for that.

Overall the picture you get is that the company has managed to stabilise costs and is in the early days of making itself into a more effective marketing machine. If the company can do that without issuing more equity and/or using more debt, then it could be a great turnaround play and a great investment for the management team.