Ruffer Asset Management put out a report earlier this year looking at market liquidity and the various risks around it. Ruffer’s ‘thing’ is developing strategies that act as something akin to a tail hedge, so doom mongering is kind of what they do.

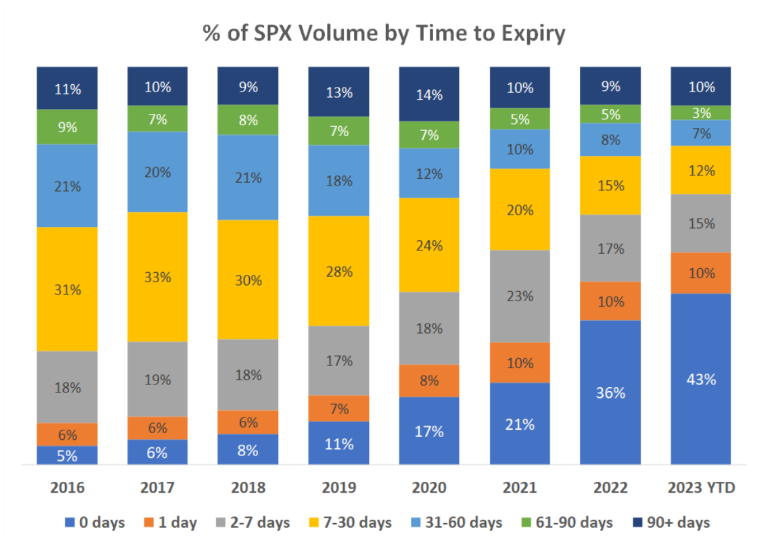

Anyway, one of the striking points was some discussion of the rise of 0dte options and their increasing share of overall volumes in options markets. I knew this had happened but was unaware to what extent. In 2023 0dte options represented close to half of all trading volume on Cboe in 2023, up from 5% in 2016.

The suggestion in Ruffer’s piece was that the hedging activity of options market makers could exacerbate volatility in underlying markets.

If you assume that’s the case then it raises an interesting question for the FX/CFD industry. The general view is that the b-book is bad primarily because (1) it creates a conflict of interest against the client and (2) it raises the likelihood of the company blowing up because of unhedged exposure.

These are fair points and I’m not disputing them but then it’s worth looking at things from the Ruffer perspective. Let’s imagine all FX/CFD trades get sent to market and are then locked in with limit orders. Does that create the potential to increase volatility and disrupt markets? And if that’s the case, is it better to keep this speculative flow warehoused and separate from people’s ISAs, 401ks and so on?

Fortunately, Cboe seems to have realised this could freak people out and is eager to allay our fears. They published some research earlier this year looking at the hedging activity of options market makers.

I won’t go into the full details but it can be summed up as…

- Volatility didn’t change much despite the dramatic increase in 0dte options trading

- This is partly because the net exposure created by options trading is low

Or in simple terms, when people trade 0dte options, there is a relatively even distribution in the combined notional value of those trades between puts and calls. The result is that there is not that much need to hedge. You can see this below…

What does this mean? As it pertains to FX/CFD trades on indices, it doesn’t seem like STP-ing all your flow would be that big a deal if your primary concern is protecting the markets from volatility.

So yes you should hedge your exposure. And then get b-booked by the market makers on exchange!